15 Mar

What are deferred tax liabilities

Deferred tax liabilities are the amounts of corporate taxes payables in future periods

In our previous article titled “difference between accounting and taxable profits”, we established that the difference between accounting and taxable profits could be of permanent and temporary nature.

Moreover, we discussed that temporary differences, which create lower taxable profits in the current period, occur due to taxable temporary differences and ultimately, it creates deferred tax liabilities.

Deferred tax liabilities are the amounts of corporate taxes payables in future periods, and this arises due to the following factors:

• Taxable revenue is lower than accounting revenue due to taxable temporary differences.

• Taxable expenses are higher than accounting expenses due to taxable temporary differences.

The tax authorities may allow businesses to pay tax on lessor income than the income booked in the statement of comprehensive income, which leads to lower taxable profits. Like interest of Dh50,000 on fixed-term deposits accrued by the A Ltd which will be received at the end of the deposit term of five years. Tax authorities will not consider this accrued interest as an income while calculating taxable profits of the current period, and the taxable temporary difference will arise due to this interest income.

In the cases where taxable expenses are higher than the accounting expenses, the typical examples are prepayments, like three years rent of Dh120,000 paid in advance. In the accounting books, it will be amortised over three years at the rate of Dh40,000 per year, while tax authorities in various jurisdictions may follow a cash basis and can ask the registered business to treat full rental payment of Dh120,000 as allowable tax expense in the first year. So, in the current period, taxable expenses would be higher by Dh80,000 due to prepaid rent.

Source:https://www.khaleejtimes.com/finance/what-are-deferred-tax-liabilities

08 Mar

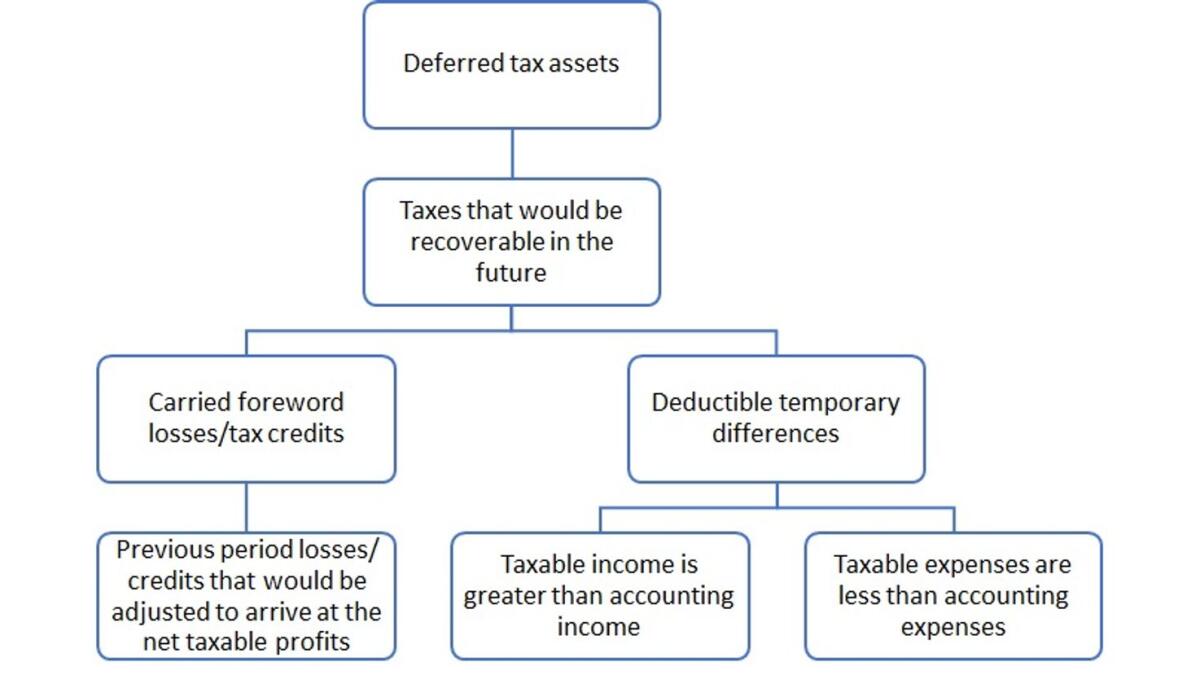

What are deferred tax assets

The tax authorities may ask businesses to pay tax on more income than the income booked in the statement of comprehensive income, which leads to more taxable profits

In our previous article titled “difference between accounting and taxable profits”, we established that the difference between accounting and taxable profits could be of permanent and temporary nature. Moreover, we discussed that temporary differences, which resulted in higher taxable profits, arose due to deductible temporary differences and ultimately, it would create deferred tax assets.

Deferred tax assets are the amounts of corporate taxes recoverable in future periods, and this arises do to the following factors:

• Taxable revenue is greater than accounting revenue due to deductible temporary differences.

• Taxable expenses are less than accounting expenses due to deductible temporary differences.

• The business has carried forward tax losses/tax credits

The tax authorities may ask businesses to pay tax on more income than the income booked in the statement of comprehensive income, which leads to more taxable profits. Like three years rent of Dh120,000 received in advance. In the accounting books, it will be amortised over three years at the rate of Dh40,000 per year, while tax authorities in various jurisdictions may follow a cash basis and can ask the registered business to treat full rental receipt of Dh120,000 as taxable income in the first year. [advances would not be subject to corporate tax in the UAE, so deferred revenue due to advances would not create any deductible temporary difference].

In the cases where taxable expenses are less than the accounting expenses, the typical examples are provision for warranties, bad debts, research and development costs, legal costs, etc. Registered businesses may book expenses on an estimated and/or provisional basis, while tax authorities may allow expenses on a cash basis. For example, A Ltd, based on the past experience, expects that three per cent of the total sales of Dh100,000 will be returned for repair in the next year and creates provision of Dh3,000 [100,000*3%]. This means A Ltd booked a liability for accrued product warranty costs by debiting expenses and crediting provision for the warranty. This provision for the warranty services may not be accepted by the tax authorities, and they may not allow related costs, which will lead to higher taxable profits, and it will become the basis for deferred tax assets.

The third reason for deferred tax assets, which will result in lower taxes in the future, is carried forwarded losses. Carried forward losses will be adjusted against the future taxable profits which will result in lower taxable profits and ultimately, it will lead to lower tax liability. The period over which losses can be carried forward vary from jurisdiction to jurisdiction, and we need to wait for the law for the exact period for which these losses can be carried forwarded.

International Financial Reporting Standards [‘IFRS’) states that deductible temporary differences are: “temporary differences that will result in amounts that are deductible in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled”.

Keeping in view the above definition of IFRS, in the aforesaid examples, rent of Dh80,000 and warranty of Dh3,000 are deductible temporary differences. The registered business will pay more tax in the current period due to these two factors. These amounts will be deductible in the future to ascertain the relevant period’s taxable profits.

IFRS with the few exceptions further states that: “a deferred tax asset shall be recognised for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilised”.

Since deductible temporary differences are Dh83,000 [80,000+3,000], so the registered business will book deferred tax asset of Dh7,470 [83,000*9% (applicable corporate tax rate)] by assuming that future taxable profits would be available against which the deductible temporary difference will be utilised.

The period in which deductible temporary differences are greater than taxable temporary differences, in that period tax expense would be lower than the tax liability, and the differential will be booked as deferred tax asset in the statement of financial position. The period in which taxable temporary differences are higher than deductible temporary differences, in that period tax expense would be higher than tax liability and the differential will be booked as deferred tax liability which we will cover in our next article.

The above understanding is based on the global practices and requirements of IFRS 12. Once the UAE government introduces corporate law, it will set a clear basis for corporate tax computation.

Source:https://www.khaleejtimes.com/finance/what-are-deferred-tax-assets

28 Feb

How to compute taxable profits in the UAE

Under the direct method of calculating taxable profits, we can calculate the taxable profits directly by deducting the cost of goods sold, tax allowable expenses and other allowable deductions from the gross income of the corporations

Our previous article focused on the differences between accounting and taxable profits. We established that permanent differences and temporary differences lead to differences in accounting profits and taxable profits. We concluded that permanent differences are incurred in one period and do not impact the subsequent period. In comparison, temporary differences are incurred in one period and affect the following period.

In this article, we will learn how to compute taxable profits. There are two approaches to calculate taxable profits, and I am naming them as (i) Direct method and (ii) Indirect method.

Under the direct method of calculating taxable profits, we can calculate the taxable profits directly by deducting the cost of goods sold, tax allowable expenses and other allowable deductions from the gross income of the corporations. Taxable income, if any would be added to arrive at the taxable profits. So, we can say that:

“Taxable Profits = Gross Income – Cost of goods sold – Tax allowable expenses and deductions + Other taxable income.”

This is a straightforward method of calculating taxable profits, and it would be very effective if the corporations were not preparing the financials regularly.

In the indirect method, taxable profit can be calculated by making accounting profits as a base, adding back all disallowable expenses, deducting tax allowable expenses, adding taxable other income, and deducting non-taxable other income. For example, the equation would be as under:

Add: Disallowable expensesXXXX

Less: Tax allowable expensesXXXX

Add: Other taxable incomeXXXX

Less: Other nontaxable income XXXX

Taxable ProfitsXXXX

Companies and tax authorities prefer to use the indirect method to calculate taxable income. This is a very effective and reliable method to compute the corporate tax where corporations are preparing the financials regularly, and these financial statements are audited by external auditors. In addition, it’s quick to calculate taxable profit as accounting profits is taken from the audited financials, and the break of other numbers is available in the notes to the financial statements.

In both of the above methods, tax allowable expenses and income are based on the principles and rules defined in the corporate tax law and related regulations.

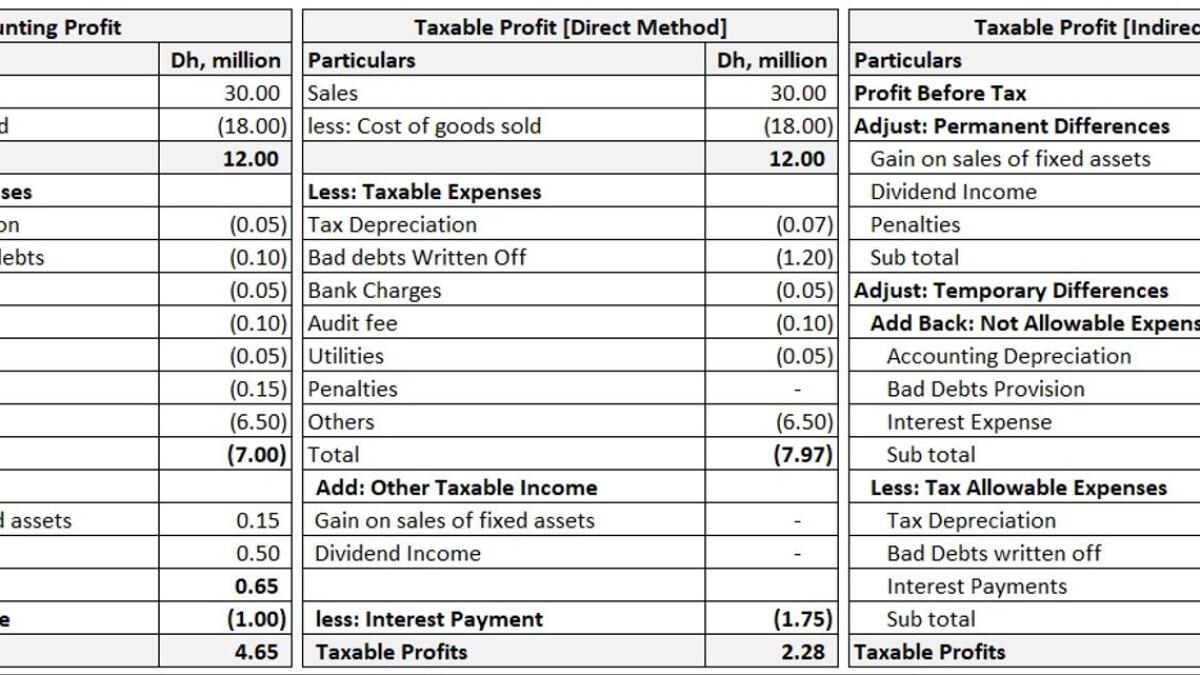

Example: ABC company has an annual income of Dh 30 million, and its cost of goods sold is Dh18 million. The company’s operative expenses are Dh7 million which includes: Accounting depreciation of Dh0.05 million while tax depreciation is Dh0.07 million; Provision for doubtful debts of Dh0.1 million while actual debts of Dh1.2 million has been written off; Bank charges Dh0.05 million, Audit fee Dh0.10 million, Utilities Dh0.05 million; Penalties Dh0.15 million, and Other expenses Dh6.5 million. The company sold a machine, and the gain was Dh0.15 million. ABC earned a dividend income of Dh0.5 million. ABC Interest expense is Dh1 million, while the actual interest payment is 1.75 million.

Solution: The diagram shows that the accounting profit before tax is Dh4.65 million while taxable profit is Dh2.28 million under both methods. Therefore, tax payable would be Dh0.21 million [Dh2.28*9 per cent].

While calculating the taxable profits, tax depreciation and bad debts written off have been allowed for tax purposes instead of accounting depreciation and provision of doubtful debts, which are not allowed for tax purposes. Penalties have not been allowed for tax purposes as an expense. Interest expense has been disallowed, while interest payment has been allowed for tax purposes. Dividend income and capital gain (gain on sale of fixed assets) are not subject to tax, so it has not been considered taxable income.

Dividend income, gain on fixed-assets sales, and penalties have created permanent differences. This means these will impact the current period, and it will not have any impact in the subsequent period. Depreciation, bad debts provision and interest have created temporary differences, and it would be offset in the following period. Both administrations have accepted bank charges, audit fees, utilities and other expenses as allowable expenses.

The above understanding is based on the global practices and press releases issued by the Ministry of UAE on corporate tax. Once introduced by the UAE government, the law and related regulations would set a clear basis for corporate tax computation.

Source:https://www.khaleejtimes.com/finance/how-to-compute-taxable-profits-in-the-uae

14 Feb

Key impacts of corporate tax on UAE businesses

Corporate tax would be the short-term liability of the businesses, which would adversely affect their working capital. Businesses would be required to assess the gap in the working capital, and they would bridge the gap

We all know that corporate tax (CT) would be effective from the financial years starting on or after June 01, 2023. All stakeholders have almost one and half years, but CT has become the talk of the town, and everyone is discussing and trying to figure out the impacts of CT on the businesses, individuals, government, and overall economy. In this article, we have assessed and analysed the impacts of CT on the key stakeholders.

Every registered business would be liable to register for CT and annually, they would be required to pay nine per cent of their adjusted taxable profits over and above the exemption threshold of Dh 375,000 so, CT would be the short-term liability of the businesses, which would adversely affect their working capital. Businesses would be required to assess the gap in the working capital, and they would bridge the gap. While preparing the budget for the respective period, companies would consider the impact of CT on the business, and they would plan the actions accordingly.

The groups which are operating in the UAE, would have an option to have single CT registration and adjust the losses of the group entities to arrive at the group taxable profits. For sure, the entities which are under common control and/or ownership would plan to go for restructuring like to change the ownership and/or control to opt-out the single CT registration, which would help them to adjust the losses of group entities and it will reduce their tax liability.

Loss-making groups or businesses would be able to carry forward their losses which would be adjusted against the future taxable profits so CT would not be considered a burden on loss-making Units.

Businesses having taxable income of up to Dh375,000 would not be subject to CT, which would incentivise start-ups and new businesses.

Alignment of the tax year with the financial year depends upon the timeline to submit the annual corporate tax return which would be announced in the law and/or the related regulations and the businesses would act accordingly.

The introduction of CT would involve implementation, training and bureaucratic compliance cost which would not be too high as the tax system is very simple in the UAE. This is certain that businesses would focus on tax planning to minimize the impact of CT on their profits which would increase the demand for tax professionals.

It’s highly likely that shareholders would try to maintain their share of profits, and they would pass on the impact of CT to the end-users in the form of increasing sales prices which would make things a little expensive for the end-users and have an adverse impact on their purchasing power. Reduction in the purchasing power would have an impact on the demand for goods and services and its trickle-down effect would be on the production and sales of the businesses which would affect the growth of the economy in the short run.

CT affects the decisions related to Foreign Direct Investment (‘FDI’), and it creates a wedge between the pretax and post-tax returns on FDI. Investors are always keen to know the direct taxes in the country in which they wanted to invest and taxes on the repatriation of profits. Since the rate announced by the government is highly competitive as compared to other countries, and double tax treaties are in place by the UAE government so, the introduction of CT would not have any major impact on FDI. Moreover, Free Zones would keep providing invectives to the businesses for a specific period as per their respective laws, so businesses will keep enjoying the benefits of the tax. Dividend and capital gains would not be subject to CT, so it would create attraction for the investor to invest in the UAE market.

As mentioned above, it’s highly likely that businesses would pass on the impacts of CT to individuals by increasing their prices, which would impact the purchasing power of the consumers. Employees would demand an increase in salaries to maintain their purchasing power. On an overall basis, goods and services would become slightly expensive for the end-users.

Globally, taxes are the major source of revenue for governments. Governments across the globe spend these taxes on the welfare of the public. In the same way, like VAT, CT would become another source of income for the Government of UAE and the UAE Government would spend this income for the welfare of the public by developing world-class infrastructure, hospitals, roads, medical facilities etc.

Moreover, it would reduce reliance on oil-generated money and lead to diversified sources of income for the Government which would be a sign of a healthy and matured economy.

Being its competitiveness, CT would have a nominal impact on the corporate savings and FDI, which would create an adverse impact on the growth of the country in the short run, but in the long run, it would develop the confidence of the investors which would lead to growth.

Keeping in view all the above, in nutshell, we can conclude that CT has been crafted to incentivize investment and keep transparency to meet global standards which would provide a stable society where businesses would contribute and add value for the growth of the economy.

Source:https://www.khaleejtimes.com/business/key-impacts-of-corporate-tax-on-uae-businesses