24 Mar

What is Fatca

The US, the Philippines, North Korea, Libya and Eritrea are some of the countries which charge a tax on the global revenue of their citizens and residents

The United States (US) is the only major country that applies a tax on the worldwide income of its citizens and tax residents. The other countries which charge a tax on the global revenue of their citizens and residents are the Philippines, North Korea, Libya and Eritrea.

If they are living abroad and earning any income, the US citizens are liable to submit the annual tax return to Internal Revenue Service (IRS). In addition, the US taxpayers who own foreign accounts are responsible for reporting those accounts to the US treasury department.

To avoid tax evasion, the US government introduced the Foreign Account Tax Compliance Act (Fatca) in 2010, which requires Foreign Financial Institutions (FFIs) to report information about financial accounts held by US taxpayers or by foreign entities in which US taxpayers have a substantial ownership interest. Unless exempt, FFIs that do not comply with the Fatca, 30 per cent withholding tax applies to their US source payments made to them.

FFIs can submit this information directly to the IRS by logging in to their portal or through the competent authority of the respective country where the Intergovernmental Agreements (IGA) are in place. Including China, 113 jurisdictions have signed the IGA to comply with Fatca, and the UAE is one of them.

The UAE signed IGA with the US government (US-UAE IGA) on June 17, 2015. Being a competent authority, the Ministry of Finance in the UAE, issued guidance on the UAE IGA on July 6, 2015.

In the IGA, both of the parties have agreed that the UAE will collect and exchange the information on each “US Reportable Account” on an annual basis with the US relevant authority, and the US Reportable Account has been defined as under in the IGA: “Financial Account maintained by a Reporting UAE Financial Institution and held by one or more Specified US Persons or by a non-US entity with one or more controlling persons that is a specified US person”.

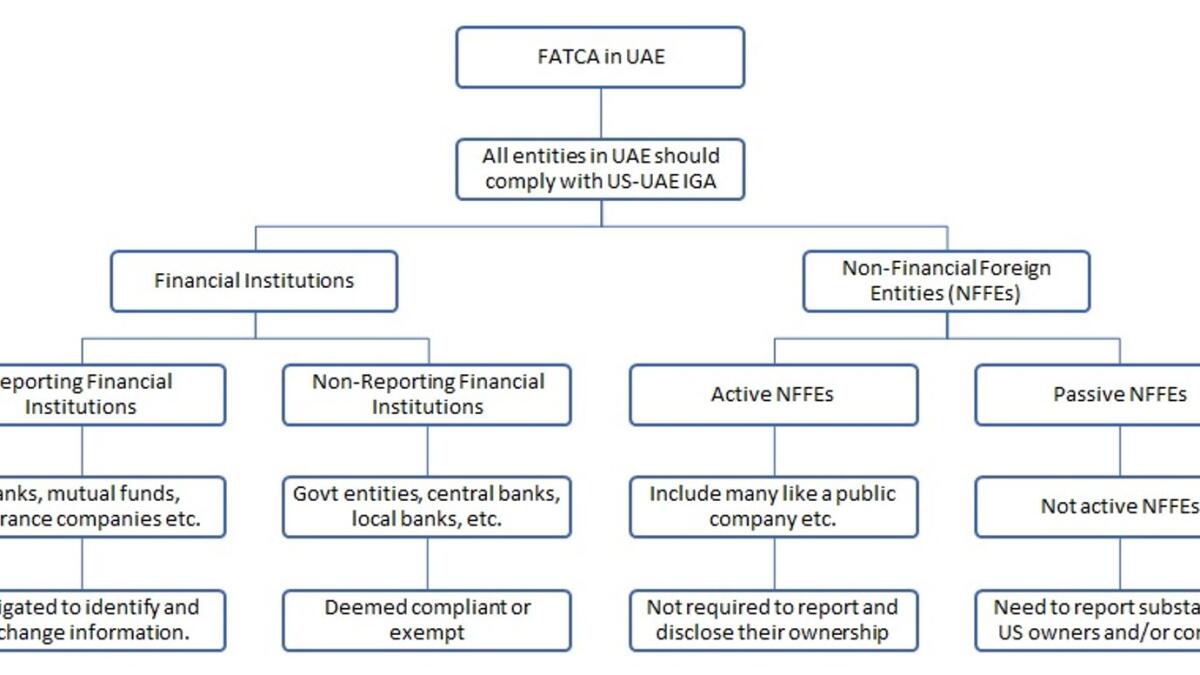

Under the UAE Law, all entities within the UAE should comply with the US-UAE IGA, and the entities can be classified into (i) Financial Institutions (FIs) and (ii) Non-Financial Foreign Entities (NFFEs).

FIs can be categorised as (i) Reporting FIs, and (ii) Non-Reporting FIs. Each reporting FI shall be treated as complying with Fatca, and 30 per cent tax will not be held on the US source payment if the related information has been provided by the UAE government within the due date and the reporting FI comply certain conditions. Each non-reporting FI shall be deemed compliant or exempt beneficial owner.

Non-reporting FIs are generally not required to report information to the UAE; however, they will need to provide properly completed US tax forms or self-certifications to avoid Fatca withholding on US source payments to them. The key example of non-reporting FIs as given in the annexure-II of US-UAE IGA are government entities, intergovernmental organizations, central bank, FIs with a local client base, local bank, FI with only low-value accounts etc.

Non-US entities that are not FIs are considered to be Non-Financial Foreign Entities (NFFEs) which can be classified as (i) Active NFFEs and (ii) Passive NFFEs.

An “Active NFFE” means any NFFE that meets any of the criteria like less than 50 per cent of their gross income is passive income and less than 50 per cent assets are held to produce passive income, the stock of the NFFE is regularly traded on an established securities market or the NFFE is a related entity of an entity the stock of which is regularly traded on an established securities market, the NFFE is a government or part of the government, the NFFE is organised in a US territory and all of the owners of the payee are bona fide residents, of that US territory; etc.

All active NFFEs doesn’t require any Fatca reporting but properly completed US tax forms or self-certification is required in order to avoid Fatca withholding on US source payments to them. Any NFFE which is not active will be considered passive NFFE. All passive NFFEs are required to identify and exchange information about their substantial US owners and/or controlling persons who are specified US persons.

Regulated entities will be regulated by their regulators. All economic department entities will be governed by the Federal Ministry of economy, and all freezone entities will be managed by the respective freezones authorities for the compliance and enforcement of Fatca.

Source:https://www.khaleejtimes.com/finance/what-is-fatca